What is it ?

The HFT_TRENDSCALPER system combines two powerful trading strategies — TrendScalping and Latency Arbitrage — into a unified platform. Designed for precision and adaptability, this system delivers consistent profitability across both trending and volatile market conditions by leveraging the strengths of its proprietary HFT_TREND engine and high-frequency trading technology.

1. TrendScalping Strategy (HFT_TREND Engine)

At the core of the TrendScalping component is the HFT_TREND engine, a next-generation system engineered to capture impulsive market movements at the onset of new trends.

Operating across both the FIX API platform and the MT4 platform, HFT_TREND enables seamless trading on virtually any broker that supports these infrastructures. Unlike conventional arbitrage bots that are often flagged by brokers, HFT_TREND is broker-friendly and engages only in sustainable, stable trading practices — avoiding toxic, high-risk methods.

The foundation of HFT_TREND lies in a sophisticated impulse trading algorithm powered by a proprietary impulse indicator developed by Nehcap. This indicator identifies a sequence of high-probability impulses — sharp movements that typically precede sustained trends — and initiates trades in the direction of these newly forming moves.

To refine trade quality and filter out false signals, the system incorporates ATR (Average True Range) indicators to dynamically assess market volatility. Trades are only initiated when volatility levels are conducive to trend continuation, enhancing the probability of successful entries.

Key elements of risk management within HFT_TREND include:

- One active position per trading instrument at a time, limiting exposure and avoiding over-trading.

- Strict avoidance of martingale or grid strategies, ensuring position sizing remains consistent without compounding losses.

- Trailing stop mechanisms for exit management, allowing profits to run while systematically locking in gains.

Additionally, HFT_TRENDSCALPER integrates a rapid feed filter, which blocks trade entries during periods of abnormal market activity, such as major news releases or sudden liquidity shifts. This keeps the TrendScalping strategy disciplined, robust, and well-insulated against erratic market behavior.

2. Latency Arbitrage Strategy

The second pillar of HFT_TRENDSCALPER is a high-frequency Latency Arbitrage module that exploits micro-second price inefficiencies between fast and slow brokers.

This strategy operates as follows:

- The system continuously monitors live quotes from a fast broker (providing quicker price updates) and a slow broker (exhibiting slight delays).

- When a discrepancy is detected — for example, if EURUSD is quoted at 1.34567 on a slow broker and 1.34540 on a fast broker — HFT_TRENDSCALPER executes a sell order on the slow broker, anticipating that the price will soon realign downward.

Key features of the Latency Arbitrage module include:

- Ultra-fast detection and execution, enabling trades to capitalize on pricing gaps before the slow broker adjusts.

- Built-in protection mechanisms against adverse spread, slippage, or network lag, ensuring only high-probability trades are executed.

- Dynamic risk controls and customizable thresholds to maintain consistent performance even during changing market conditions.

These measures render dishonest broker practices futile, while deposit insurance mandates rigorous oversight from regulators to ensure client protection.

Installation

Once the investors buys the system, our team will take care of full installation and day to day support. This system is life time free updates and support.

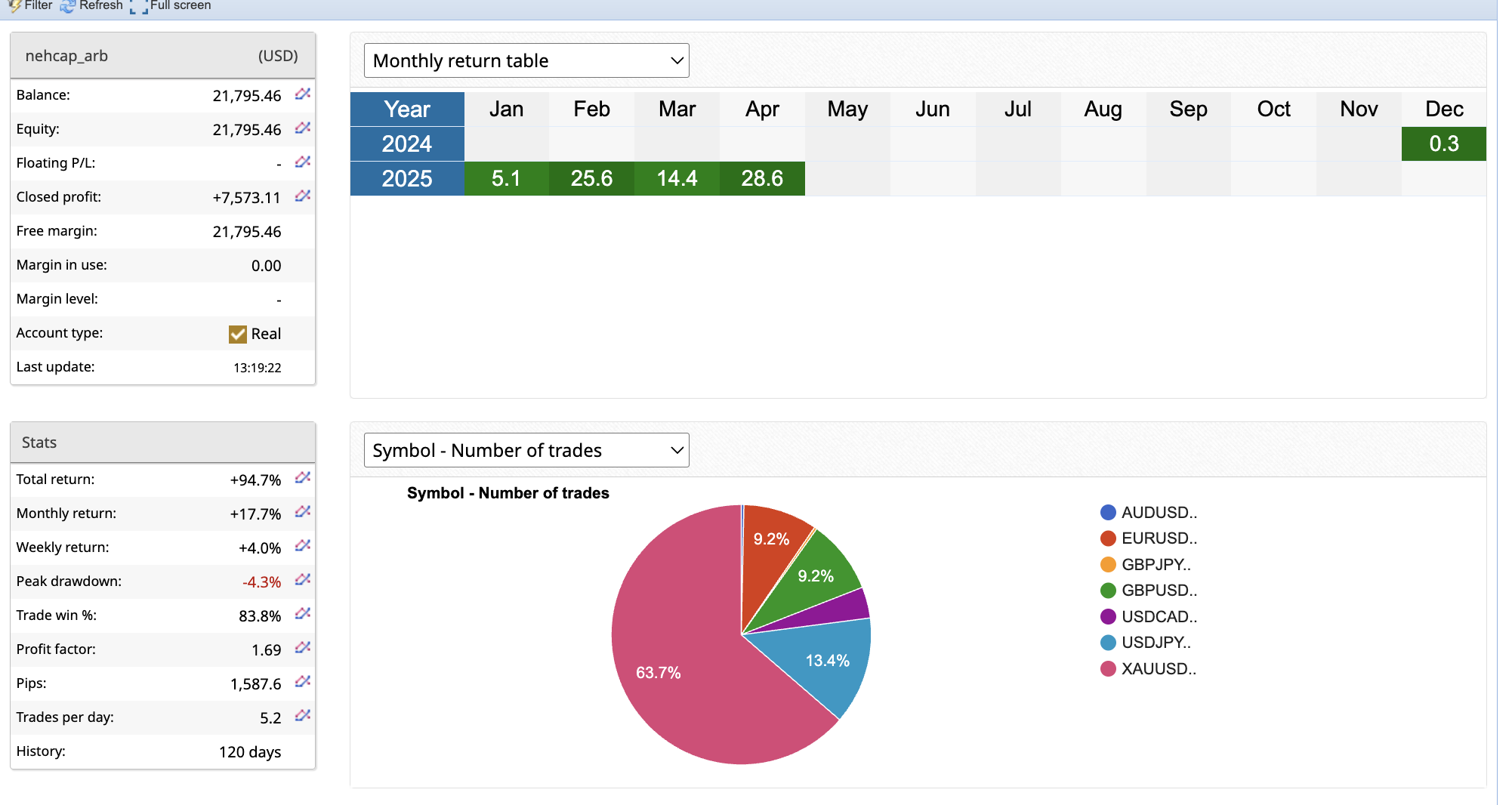

Performance

Cost

How to start

Step 1: Please open a FIX based account or MT4 ECN account from below at either of them. PFD is a free broker while VARIANSE Is a paid broker for offering its PRIME-XM account which is highly recommended for HFT systems. You can open an account at either broker below.

- OPEN A NEW LIVE CCOUNT at Pacific Financial Derivatives

- OPEN A NEW ACCOUNT at Varianse Broker (UK regulated) (Highest tickdensity)

- OPEN A NEW ACCOUNT at ROBOFOREX Broker

- OPEN A NEW ACCOUNT at VANTAGEMARKETS Broker

Step 2: Deposit the funds you want to trade.

Step 3: Submit your FIX/MT4 details via email support@nehcap.com or telegram @mqlnehcap

Step 4: Trading commences after client submits risk parameters like lot sizes and so on.

To start. send a request by clicking submit below

[ninja_form id=12]