High frequency trading is not simply fast trading. It is a different way of interacting with market structure. The system is designed to read price, liquidity, venue response and execution state faster than a normal discretionary or retail platform can observe and respond.

In fast FX and gold conditions, the difference between 10 milliseconds and 600 milliseconds can be the difference between participating in the first executable price and arriving after the move has already repriced. This is why execution architecture matters as much as signal logic.

Why HFT Sees The Market Before Retail Reacts

A retail trader normally sees the market after several steps have already happened: liquidity providers update pricing, the broker updates the platform, the chart refreshes, the trader interprets the move, the order is clicked or sent by an EA, and the broker then routes or internalises the order. That sequence can easily move into several hundred milliseconds.

A high frequency system is built differently. It can consume tick or liquidity changes directly, process the rule set instantly, transmit a FIX order, receive an acknowledgement and decide whether to continue, cancel or exit while the broader market is still reacting. In a news-release environment, that timing gap is critical.

The important point is not that speed creates profit by itself. Speed gives the system the right to compete for the first liquidity. Whether that becomes profitable depends on the quality of the signal, the fill logic, the rejection logic, position limits, spread filters and the ability to step aside when conditions are no longer favourable.

The News-Release Timing Problem

During a scheduled news event, price can reprice in layers. The first layer is the immediate liquidity adjustment. The second layer is the spread widening and broker/platform update. The third layer is the retail reaction, where traders see the candle move and attempt to join the direction.

A true HFT model attempts to operate inside the first layer. It may send a Fill-Or-Kill order through FIX, take only the price it is willing to accept, and reject the trade if execution quality is not available. By the time a retail trader presses buy or sell, the HFT system may have already entered, repriced risk, or fully exited.

This is why many retail news traders experience slippage. They are not competing against the candle they see. They are competing against systems that have already responded to the tick event before the candle is visually useful.

Execution Speed: 10 ms Versus 600 ms

In a well-built HFT environment, round-trip execution can target approximately 10 milliseconds in favourable infrastructure conditions. This normally requires a low-latency FIX connection, disciplined order logic, suitable server placement and broker infrastructure close to liquidity.

Retail trading is structurally slower. A desktop or mobile order path can move above 600 milliseconds once chart refresh, terminal processing, user reaction, broker bridge, liquidity response and confirmation are included. Even a normal VPS EA can still be materially slower than an optimized FIX stack.

That speed difference changes the trade. At 10 ms, the system may still be trading the initial imbalance. At 600 ms, the trader may be paying for the move after the opportunity has already been repriced.

Why FIX And FOK Matter

FIX API is commonly used in professional execution because it is designed for direct, structured message flow between trading systems and counterparties. It avoids much of the visual platform overhead that retail traders associate with MT4 or MT5.

Fill-Or-Kill execution is important in fast markets because it defines the trade condition clearly: fill the order at the accepted terms, or do not fill it. This can protect a high-speed system from accepting a late or distorted price after the edge has disappeared.

For high frequency models, a rejected order is often better than a poor fill. A system that accepts every fill may appear active, but it can transfer edge to the broker, bridge or liquidity provider through slippage and delayed execution.

Main Types Of High Frequency Trading Systems

- News reaction systems: attempt to capture rapid repricing after scheduled economic releases or unscheduled market shocks.

- Latency arbitrage systems: compare faster and slower price streams, seeking execution before a delayed venue fully updates.

- Market-making systems: quote both sides of the market and manage inventory, spread capture and adverse selection risk.

- Order-book imbalance systems: read liquidity pressure and attempt to trade short-lived directional pressure.

- Statistical arbitrage systems: act on temporary dislocations between correlated instruments or venues.

- High-speed trend-burst systems: react to structural breaks, support/resistance shifts and rapid momentum expansion.

Each type has a different risk profile. News reaction depends on event timing and spread behaviour. Latency arbitrage depends on feed quality and venue acceptance. Market making depends on inventory control. Trend-burst systems depend on recognising when a level has changed from passive structure into active momentum.

Where HFT_FIX And CREST Fit

HFT_FIX is NEHCap’s FIX-engine high-frequency FX framework. Its focus is execution speed, FOK order handling and fast participation across major FX and gold conditions where milliseconds can materially affect entry quality.

CREST is a high-speed support/resistance trend-burst system. It is not the same as a pure tick-arbitrage engine, but it belongs in the same execution-sensitive family because its opportunity comes from reacting quickly when market structure changes and momentum expands from a level.

The distinction matters. HFT_FIX is primarily an execution-speed framework. CREST is a structural reaction framework. Both require discipline around latency, broker conditions, symbol behaviour, risk limits and live account monitoring.

Why Most Retail Traders Cannot Replicate HFT Manually

The retail trader sees a candle. The HFT system sees a sequence of ticks, spread changes, acknowledgement times, rejection rates and liquidity behaviour. By the time the candle looks obvious, the microstructure opportunity may already be gone.

This is why professional evaluation of HFT systems should focus on live account evidence, execution records, drawdown, account age and withdrawal history. A strategy that depends on speed must be proven in live conditions because backtests cannot fully represent rejection, slippage, spread expansion or broker-side routing.

What Investors Should Check In An HFT System

- Live account history rather than only backtest curves.

- Execution venue, server location and broker infrastructure.

- Order type logic, including how the system handles rejection and slippage.

- Drawdown behaviour during volatile sessions.

- Trade frequency and whether returns come from repeatable conditions.

- Whether the system continues to function after withdrawals, scaling and changing market regimes.

The Practical Lesson

High frequency trading is an infrastructure game and a risk-control game before it is a signal game. The signal has to be fast, but the execution path has to be faster. The system must know when to trade, when to reject, and when not to participate.

For investors, the correct question is not simply whether a system is fast. The better question is whether speed is being converted into controlled live-account performance under real broker conditions.

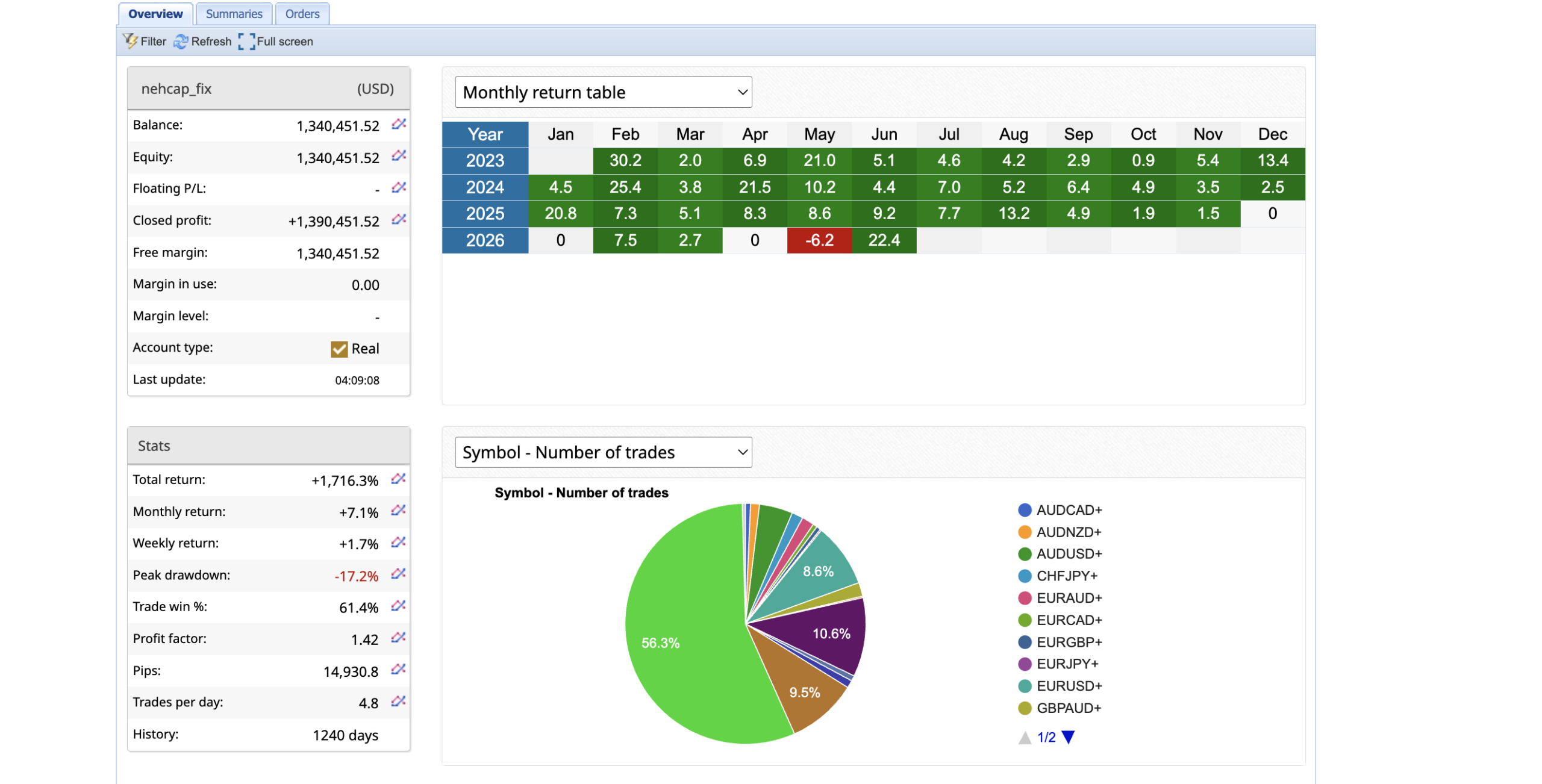

NEHCap operates three live trading frameworks across high-frequency FX, arbitrage execution and high-speed trend systems:

- HFT_FIX – FIX-engine high-frequency FX model, with the latest performance snapshot shown here.

- NEDEX – masked arbitrage framework designed for short-lived pricing inefficiencies; available for MT4, MT5 and FIX API discussion.

- CREST – high-speed support/resistance trend-burst system; available for MT4, MT5 and FIX API discussion.

Contact NEHCap or message Telegram: @mqlnehcap / t.me/nehcapmeta.

This material is provided for education and market understanding only. It is not personal investment advice, a recommendation to trade, or a guarantee of future performance.